Table of contents

2. Where has Beijing directed its overseas financing for ports and equipment?

2.1 Chinese-financed ports in high-income countries

2.1.1 Regional focus: Oceania and Australia

2.1.2 Regional focus: The Middle East

3. Chinese-financed port equipment: Linking hardware and software

3.1 What accounts for China’s increased financing of ports equipment?

3.2 Which Chinese entities provide port equipment?

3.3 Why port equipment should be evaluated alongside general port financing

4. China’s shifting maritime strategy: From overt basing to hubs of connectivity

4.1 A change in China’s strategy: Keeping a lower profile?

4.2 Hubs of connectivity: Integrating the port-railway-mine model

4.2.1 Co-locating seaports with Chinese-financed critical mineral operations

4.3 A case study for China’s new approach: Linking Brazil and Peru

Case study: Port of Morébaya, Guinea

5. Implications of Chinese naval developments

6. China’s naval activity at global seaports

6.1 Chinese overseas basing and military installations

6.2 Quantifying Chinese naval activity at Chinese-financed seaports overseas

6.3 Tracking Chinese hospital ship diplomacy

Case study: China’s Arctic interests

7. Implications for U.S. maritime and economic statecraft

7.3 Ports in the United States: A case study of the Hampton Roads region

8. Conclusion and recommendations

8.1 The U.S. and its allies must develop a long-term strategy

Overseas ports projects under development or in China’s financing pipeline

8.2 Port construction is just one piece of the puzzle, requiring holistic thinking

8.3 Countries that host ports must be empowered to better screen investments

8.4 Establish a taskforce or research center on China’s overseas seaports

Figures

Figure 1a. Port of Tema in 2016, before new development5

Figure 1b. Port of Tema in Ghana in 2024, prior to opening in 20255

Figure 2. China’s official sector lending and grant-giving for overseas ports, 2000-20259

Figure 3. Breakdown of Chinese-financed seaport projects by Chinese entity involvement12

Table 3. Chinese ports financing by top funding agencies and recipient countries, 2000-202514

Figure 4b. Lekki Deep Sea Port in 2024, after opening in 202317

Figure 5a. Khalifa Port in 2016, prior to Chinese-financed development26

Figure 5b. Khalifa Port in 2021, after Terminal 2’s opening in 201926

Figure 6. Chinese official financing for overseas port equipment, 2000-202530

Figure 7. Chinese official financing for port equipment by type, 2000-202532

Figure 8. Composition of Chinese port equipment providers by implementing agency, 2000-202333

Figure 10. Colocation of Chinese-financed seaport and mining projects, 2000-202342

Figure 11a. Site of the future Chancay Port in 2018, prior to development45

Figure 11b. Chancay Port in 2025, after opening in late 202445

Figure 12. The Brazil-Peru Bioceanic Corridor and Porto Sul construction plans46

Figure 13. Chinese-financed ports with Chinese naval activity pre- or post-financing, 2000-202558

Figure 14. Chinese financing by type for ports with Chinese naval activity pre- or post-financing60

Figure 18. A proposed “Port Shopper Tool” to navigate port financing and deals96

Tables

Table 1. Top 20 Chinese-financed ports, 2000-202510

Table 2. Financing for ports and port facilities with both Chinese owners and operators, 2000-202513

Table 3. Chinese ports financing by top funding agencies and recipient countries, 2000-202514

Table 4. Top 10 Chinese-financed ports during the late BRI, 2018-202516

Table 5. Top 20 Chinese-financed ports in high-income countries, 2000-202519

Table 6. Examples of five areas of security sought out by Chinese companies and agencies40

Table 7. Examples of co-located Chinese-financed seaports and mines43

Anchoring Global Ambitions

Beijing’s Ports Financing and the Race for Maritime Dominance

By Alexander Wooley, Lea Thome, Sheng Zhang, Rory Fedorochko, Sarina Patterson, and Seth Goodman

Acknowledgments

This report was prepared by Alexander Wooley, Lea Thome, Sheng Zhang, Rory Fedorochko, Sarina Patterson, and Seth Goodman. Our analysis draws upon a newly assembled dataset—the Chinese-financed Ports Overseas and Related Terminals Dataset, Version 2.0 (CPORTS 2.0)—released by AidData in conjunction with this report.

We owe a major debt of gratitude to AidData’s Tracking Underreported Financial Flows (TUFF) Unit and the international network of researchers—including Bradley C. Parks, Brooke Escobar, Katherine Walsh, Sheng Zhang, Rory Fedorochko, Lydia Vlasto, Julie Sickell, Sailor Miao, Emma Bury, Jacqueline Zimmerman, Samantha Custer, Axel Dreher, Lukas Franz, Andreas Fuchs, Sebastian Horn, Ammar A. Malik, Carmen M. Reinhart, Austin Strange, Michael J. Tierney, and Christoph Trebesch—who developed the latest version of the TUFF methodology and AidData’s China’s Global Loans and Grants Dataset, Version 1.0 (CLG-Global 1.0). We are also grateful to the authors—Bradley C. Parks, Sheng Zhang, Brooke Escobar, Katherine Walsh, Rory Fedorochko, Lydia Vlasto, Jacqueline Zimmerman, Julie Sickell, Emma Bury, Ameya Joshi, Lea Thome, Oshin Pandey, and Pavan Raghavendra Raja Manuri Venkata—of a related report, Chasing China: Learning to Play by Beijing's Global Lending Rules, which informed our analysis. Our work was supported as well by research assistant Ian Harman, who developed variable definitions, manually coded variables, formatted references, and conducted a qualitative literature review; we are grateful for his contributions.

A large team of AidData research assistants also provided invaluable support, including Abena Konadu, Akash Nayak, Aldrin Yashko, Alejandro Schnapp Mezerhane, Alexis Dolack, Allison Swindell, Amelia Smith, Amruta Veer, Amy Browning, Andy Shufer, Anna Garrett, Anna Wood, Anne Paxton, Araella Bruerd, Arianna LaGamma, Audra Killian, Bailey Nicholson, Bemnet Legesse, Benjamin Fu, Benjamin Greenberg, Beyoncé Lightfoot, Caitlyn Phung, Cameron (Bailey) Garber, Carina Rosenberg, Caroline Elszy, Carter Danto, Chelsea Wright, Chenglin Gong, Christina Wu, Claire Rudinsky, Claire Wyszynski, Clara McAllister, Colin Mullee, Collin Absher, Conrad Bruton, Cy Strain-Seymour, David Zhu, Davide Zoppolato, Dazhong Cui, Dingyi He, Dory Gilmer, Eesha Kulkarni, Emily Tchorz, Emma O'Horo, Emma Williams, Eric Montesi, Ethan Robertson, Gabriella Flores, George Beck, George (Teddy) Chunias, Grace Dorion, Grace McGehee, Grace Rosenberg, Gujie Shen, Gwyneth Smith, Hana Keenan, Haoyu (Kevin) Leng, Hari Hara Nagarjuna Raavi, Harrison Abramsohn, Helen Tieder, Henry Freytag, Henry Hubbard, Henry Tieder, Ian Harman, Ian Kung, Ihsan Amin, Isaac Herzog, Jaclyn Velotas, Jackson Humphreys, Jennifer Twark, Jiexi Lin, John Keating, Josep Ocampo, Julia Beverley, Julia Swearer, Justin Ober, Kaito Elston, Katelyn Oxer, Kelly Shinners, Kyurhee Kim, Lauren Creed, Lebron Parsell, Liang Geng, Lillian Butler, Maggie Blake, Man-Hsuan (Annie) Lin, Marianna Bonilla, Max Berckmueller, Meveryn Chua, Michael Olyniec, Prabhdeep Singh, Prestin Tran, Radhika Rohit, Rebeca Uranga, Redmond Scales, Regina Chaillo, Riley Companion, Ronan Gormley, Sabrina Levri, Samantha Rofman, Samuel Li, Saoirse O'Hair, Sarah Kennedy, Saranga Bansal, Sean Nguyen, Sebastian Meier, Shannon McGuire, Shiying Cai, Spencer Krivo, Stephen Moreau, Summer King, Supriya Navnith, Taylor Perry, Victor Gedeck, Vikhyat Kethamukkala, Violet Shi, Westley Jacanin, William Olichney, Xingyun (Ella) Pan, Ye Xiao, Yusuf Gunter-Rahman, Yuxi (Felix) Tian, Yuxuan (Flora) Wu, Zachary McClure, Zhuangqi (Steven) Zheng, and Zupeng Zeng.

Additionally, we thank the experts who kindly shared their time and insights at various stages throughout this project, including the following peer reviewers: Bradley C. Parks, AidData’s Executive Director; Brooke Escobar, AidData’s Director of the Tracking Underrepresented Financial Flows (TUFF) Unit; the executive of a global shipping company; the recently retired CEO of a major port in Asia; Michael Fabey, author and naval journalist for Janes; Jhih-Siang Liu, Assistant Professor, National Defense University, Taiwan; and Wendy Leutert, Associate Professor, Indiana University. We are also grateful to Wood Mackenzie Vesseltracker for generously providing maritime traffic data that informed this analysis. We also extend our gratitude to John Custer, who formatted the dataset and created data visualizations and the forthcoming HTML version of this report. Sarina Patterson edited and formatted the report and designed the cover; the cover image is by rjankovsky via Adobe Stock, used under the Standard license.

We gratefully acknowledge financial support from the William and Flora Hewlett Foundation and the Smith Richardson Foundation. The findings, interpretations, and conclusions expressed in this study are entirely those of the authors, and they do not necessarily represent the views of the William and Flora Hewlett Foundation or the Smith Richardson Foundation. AidData’s research is guided by the principles of independence, integrity, transparency, and rigor. A diverse group of funders supports AidData’s work, but they do not determine its research findings or recommendations.

Citation

Report

Wooley, A., Thome, L., Zhang, S., Fedorochko, R., S. Patterson and Goodman, S. 2026. Anchoring Global Ambitions: Beijing’s Ports Financing and the Race for Global Maritime Dominance. Williamsburg, VA: AidData at William & Mary.

Dataset

Thome, L., Fedorochko, R., and Zhang, S. 2026. Chinese-Financed Ports Overseas and Related Terminals (CPORTS) Dataset, Version 2.0, 2000-2025. Retrieved from: www.aiddata.org/data/chinas-official-seaport-finance-dataset-2000-2023.

Author Contribution Statement

A.W., L.T.,S.Z., R.F., and S.P. conceptualized and planned this report, beginning in 2024. S.Z., R.F., and L.T. collected the data used in the analysis. L.T., S.Z., and R.F. led the analysis of the data. S.G. provided and analyzed the geospatial imagery. S.P. and A.W. edited this report. All authors contributed to the preparation of the manuscript.

About the authors

Alexander Wooley is Director of Partnerships and Communications at AidData. He was the lead author of the Harboring Global Ambitions report that examined China’s global ports footprint and the implications for future naval bases. He has written on maritime affairs for Foreign Policy, Foreign Affairs and the U.S. Naval Institute’s Proceedings. Alex is a former section editor of the Georgetown Journal of International Affairs and a former officer in the British Royal Navy. He holds an MA in Security Studies from Georgetown University.

Lea Thome is a Program Manager at AidData, where she focuses on short-form analysis and China’s financing for national security and military purposes. She holds a bachelor’s degree in Political Science and International Relations from the University of Rochester and a master’s degree in Global Affairs from Schwarzman College at Tsinghua University. Before joining AidData, she was the Schwarzman Fellow at the Wilson Center’s Kissinger Institute on China and the U.S. and a Visiting Fellow at the Institute for National Defense and Security Research.

Sheng Zhang is a Senior Research Analyst for the Chinese Development Finance Program at AidData, where he focuses on development finance, infrastructure investment, critical minerals, and Environmental, Social, and Governance (ESG) research. His expertise guides the program’s research analysis, contributing significantly to understanding and improving sustainable development and investment practices worldwide.

Rory Fedorochko is a Program Manager with AidData’s Chinese Development Finance Program team, where he oversees the assembly of its dataset on Chinese loans and grants to high-income countries and assists on its analysis and provides a wide variety of support to other research activities of the team, including on its flagship reports and research on critical minerals and renewable energy. He previously contributed to AidData’s report on China’s ports financing, Harboring Global Ambitions.

Sarina Patterson is AidData’s Communications Manager and a co-author of Harboring Global Ambitions, a report that examined China’s global ports footprint and the implications for future naval bases. She designs and creates content for AidData’s web and social media presence, including interactive data visualizations, maps, and dashboards. She holds a BA in Government with a secondary in East Asian Studies from Harvard University.

Dr. Seth Goodman is a Research Scientist within AidData’s Research & Evaluation Unit, where he specializes in the design and operationalization of research and analysis utilizing geospatial data, machine learning, and distributed computing. Seth developed GeoQuery, AidData’s free spatial data platform, and his recent work includes exploring the use of ML-based outcome measures derived from satellite imagery, as well as assessing the efficacy of deforestation detection solutions being used to comply with the EU’s Deforestation Regulations.

Executive summary

Between 2000 and 2025, China committed nearly $24 billion in seaport-related financing supporting 168 ports across 90 low-, middle-, and high-income countries, reaching nearly every corner of the world with its official sector financing. The Anchoring Global Ambitions report and a new dataset—the Chinese-Financed Ports Overseas and Related Terminals Dataset, Version 2.0 (CPORTS 2.0)—build upon a previous investigation into Beijing’s provision of aid and credit for seaports in low- and middle-income countries (Wooley et al 2023).

Key findings include:

- Top-financed ports: Chinese state-owned creditors and donors have bankrolled over 363 seaport-related projects and activities at 168 ports around the globe. The most heavily-financed ports include Hambantota International Port ($1.97 billion), the Port of Newcastle ($1.32 billion), the Autonomous Port of Kribi ($1.17 billion), the Port of Melbourne ($1.14 billion), and Haifa Port ($1.13) billion. 2024 and 2025 alone saw $614 million of new official sector financing commitments from China for new projects and activities across eleven global ports.

- High-income countries: Chinese financing for global seaports is almost evenly split between high-income countries and low- and middle-income countries. 45.1% of its entire overseas seaport finance portfolio (worth $10.8 billion) supports 29 port locations across 20 high-income countries including Spain, Australia, New Zealand, Singapore, and Brunei.

- Combining hardware with software: In addition to extending aid and credit for the construction, expansion, and modernization of seaport facilities, Chinese state-owned financiers often support the provision of port equipment monetarily, such as security scanners or cranes provided by companies like Nuctech or ZPMC. This analysis identifies $4.7 billion in financial commitments for seaport projects that include such equipment.

- Port-railway-mine corridors: Chinese state-owned creditors and donors increasingly co-locate their port investments with other investments vital for China’s national security, such as critical mineral operations. This report identifies 19 Chinese-financed mines within a 500-kilometer radius of Chinese-financed seaports and focuses on two key case studies: the Port of Chancay and the Port of Morébaya.

- Dual-use activity: Chinese naval activity (including port calls, hospital ship visits, and joint exercises) has taken place in more than 50% of Chinese-financed port facilities where there is also a Chinese owner. There is substantially less Chinese naval activity in Chinese-financed port facilities that are not owned or operated by Chinese entities.

- New port projects in the pipeline: In addition to tracking confirmed commitments, this study identifies another $11.6 billion of pledged financing for potential or future projects at 30 ports, including Mongla Port in Bangladesh and Kisumu Port in Kenya. Also uncovered are seven new proposed port projects that fall outside the scope of this dataset but should be monitored, including Lobito Port in Angola, Sandino Port in Nicaragua, and Mubarak Al-Kabeer Port in Kuwait.

- Consequences for the U.S. and other countries: China’s nearly ubiquitous presence in the world’s top ports means that the U.S. cannot insulate itself from Chinese supply chains, in either peacetime or conflict. It must be selective about where it chooses to compete and on what dimensions. The U.S. has the opportunity to prioritize and encourage maritime prosperity zones, as set forward in the new U.S. Maritime Action Plan, including in the Hampton Roads area.

Based on newly collected data, this study makes the following policy recommendations for the host countries of port investments, policymakers, officials, and scholars:

- Policy: Encourage the U.S. and its allies to develop a long-term overseas port financing strategy.

- Plan: Incentivize holistic planning and integration of port planning with other critical aspects of the maritime domain, including operations, supply lines, shipping and shipbuilding.

- Partner: Work with host governments and beneficiaries to develop domestic policy assessment tools for incoming offers of port investments and port management.

- Platform: Establish a taskforce to produce high-quality impactful research, assessments, and recommendations.

1. Introduction

By Alexander Wooley

For over a dozen years, AidData, a research lab at William & Mary, has conducted data collection and research on China’s provision of aid and credit for overseas projects and activities. Initially this effort focused on Chinese loans and grants to Africa; it later expanded to the entire developing world. By the end of 2025, AidData was tracking Chinese official sector financing for projects and activities across 217 countries and territories in the developed and developing world—in nearly every jurisdiction other than China itself. This enormous, year-round effort is led by a team of 16 William & Mary faculty and staff and more than 120 research assistants working in twelve languages. The resulting data and analysis are made publicly available for free and for anyone to use.[1]

AidData’s latest report on China’s overseas financing portfolio, Chasing China: Learning to Play by Beijing's Global Lending Rules, was over three years in the making (Parks et al. 2025a). The accompanying dataset, China’s Global Loans and Grants Dataset, Version 1.0 (CLG-Global 1.0), is the most comprehensive and granular of its kind. It tracks more than 33,580 projects and activities across 217 countries supported by $2.2 trillion in grants and loans from more than 1,100 official sector institutions (e.g., government agencies, state-owned banks, and state-owned enterprises) in China over a 24-year period from 2000 to 2023 (Parks et al. 2025b; Dreher at el. 2022).[2]

The authors of this report, Anchoring Global Ambitions: Beijing’s Ports Financing and the Race for Maritime Dominance, are a group of AidData researchers with a special interest in maritime affairs. This study draws from and expands upon AidData’s CLG-Global 1.0 dataset to explore a topic critical to global trade and security: China’s official sector financing for overseas port projects.

For this analysis, the authors assembled a new custom dataset and conducted supplementary coding, verification, and quality assurance of data on grant- and loan-financed port projects and activities around the globe. This data collection effort was supplemented by satellite imagery for targeted geospatial analysis and deep dives into specific case studies.

The following study builds upon a previous version of port financing dataset and an earlier 2023 report, Harboring Global Ambitions: China's Ports Footprint and Implications for Future Overseas Naval Bases, that has been cited by Congressional Research Service reports (O’Rourke 2025) and described as “foundational” research on China’s global ports financing by think tanks (Sadler 2025c). In 2026, an updated version of Harboring Global Ambitions will be included as a chapter in a peer-reviewed book published by Harvard University Press.

The new Anchoring Global Ambitions report and its associated dataset—the Chinese-Financed Ports Overseas and Related Terminals Dataset, Version 2.0 (CPORTS 2.0)—go beyond earlier work to provide:

- Temporal coverage of official Chinese grant- and loan-financed seaport projects and activities from 2000 through 2025, making it the most comprehensive, publicly available dataset to provide a near-real-time picture of China’s global ports footprint;

- Global coverage of 217 countries, including both high-income and developing countries; and

- The inclusion of port equipment projects and activities, including those involving the acquisition and installation of shoreside cranes and scanners.

The CPORTS 2.0 dataset is the largest of its kind on China’s official lending and grant-giving for overseas port construction, expansion, and related infrastructure activities—with more than double the number of records in the 1.0 dataset. CPORTS 2.0 contains 129 variables for each record, providing granular information on precise project locations; financial commitment amounts and currencies of denomination; financing, co-financing, implementing, and receiving agencies; project status determinations; countries of activity (where the financed projects or activities take place); countries of incorporation (where the direct receiving agencies of the financial or in-kind transfers are legally incorporated); planned and actual commitment, implementation, and completion dates; borrowing terms (including information on the maturities, interest rates, grace periods, grant elements, and sources of collateral); and detailed narrative descriptions. Additionally, the CPORTS 2.0 dataset contains 29 unique variables not found in the AidData CLG-Global 1.0 dataset—including information on the specific type and purpose of financing for ports and equipment; prior Chinese naval activity at ports (including port calls, hospital ship visits, and joint exercises); and the presence of Chinese state-financed mines near ports.

In total, this analysis finds 363 Chinese loan- and grant-financed projects worth $23.9 billion (in 2025 U.S. dollars) supporting 168 unique ports across 90 countries from 2000 to 2025.[3] 159 projects supported by commitments worth $10.8 billion are located in high-income countries (HICs), while 204 projects supported by commitments worth $13.1 billion are located in low- and middle-income countries (LMICs).

Importantly, the CPORTS 2.0 dataset provides a precise timeline for each port project, including dates for the pledge, commitment, commencement, and completion of each project over a 26-year period (2000-2025). Thus, while much of this report examines China’s financial commitments for port projects, the dataset can also be used to track subsequent implementation activities and milestones. The satellite imagery used in this report captures ports both prior to the receipt of a financial commitment from China and post-implementation, enabling before-and-after analysis. Since the CPORTS 2.0 dataset includes information on port financing commitments through the end of 2025 (and thus beyond the 2000-2023 period of coverage found in AidData’s CLG-Global 1.0 dataset), it also tracks commitments that have only recently been made or announced and projects where construction is still new or in progress.

This report and the CPORTS 2.0 dataset therefore present the clearest picture yet of the geographic distribution and strategic intent behind China’s global maritime footprint. Previous studies by economists, political scientists, and lawyers from AidData, the Center for Global Development, the Kiel Institute for the World Economy, and the Peterson Institute for International Economics have found little empirical evidence for the “debt trap diplomacy” narrative, which has quickly become an article of faith in Western capitals(Parks et al. 2022; Gelpern et al. 2023, 2025a, forthcoming). Our findings strengthen the argument that Beijing does not seek sovereign control of physical assets in overseas jurisdictions as much as it seeks strategic security, built upon key points of access connected through channels of trade, communication, capital and influence. To date, there is little evidence that China is prioritizing the overt militarization of ports with the intent of converting or using existing ports as major naval bases, though this possibility cannot be ruled out. Instead, China is investing in ports that can receive its vast exports and facilitate the movement of essential commodities, such as critical minerals, liquid natural gas, oil, soybeans and other food products, and more. These ports are designed to promote Chinese commercial interests overseas and maximize profits for its lenders.

However, this focus on economic and commercial pursuits is happening at the same time as China’s navy, the People’s Liberation Army Navy (PLAN), is undergoing significant growth and technological development, as described in Chapter 5 of this report. China’s global maritime supply chains, anchored by its overseas port network, provide a major geopolitical benefit: a parallel logistic network that offers Beijing strategic independence, free from interference from Western institutions, and permits it to contemplate a military counter to possible island chain containment strategies or constricting blockades attempted by an enemy in any future conflict.

Interspersed throughout this study are satellite images showing the construction and expansion of Chinese-financed overseas ports, such as the Port of Tema in Figures 1a and 1b below. What is striking is not only the sheer size of new port construction, but also the development of associated infrastructure shore—including vast swathes of built-up industrial and transportation infrastructure and residential areas. In many cases, major ports have arisen along coastlines off the beaten path where there was little infrastructure previously, re-fashioning the landscape and reshaping trade patterns.

Figure 1a. Port of Tema in 2016, before new development

Figure 1b. Port of Tema in Ghana in 2024, prior to opening in 2025

Sources: Imagery in Figures 1a and 1b by Airbus (2025) and Google Earth.

A broader lesson of this study is that for most of the world’s powers (and especially for China, the United States, and the EU), economic statecraft, domestic industrial policy, and national security are now more closely intertwined than perhaps since World War II. Here, again, China has an advantage—with a long history of supporting state-sponsored or subsidized shipbuilding and shipping, as well as related infrastructure. Commercial shipping companies, meanwhile, typically prefer to follow the money and avoid choosing sides in great power competition. Yet in this changing environment, they may be increasingly forced into alignment with a given power’s national interests.

Beyond just the commercial value of these investments, many ports captured by the CPORTS 2.0 dataset lie on critical sea lines of communication (SLOCs)—ones which Beijing could determine are worth defending in times of conflict, crisis, or contingency. A port is only a starting or end-point for maritime traffic, and this study therefore also touches on the growing overland infrastructure that brings critical commodities to Chinese-funded overseas ports for onward shipment to the Chinese mainland. While Chinese port construction and expansion is re-shaping and re-defining trade routes, other forces will drive maritime trade routes and traffic over the coming decade. These include tit-for-tat tariffs; export controls on critical minerals, the vast bulk of which travel by ship; increased and targeted port fees; the opening up of polar shipping lanes; and the possibility of conflict at maritime chokepoints (such as the recent Houthi attacks on the Suez Canal or disruptions in the Strait of Hormuz) that shut down or severely reduce traffic for an extended period.

This report’s publication comes at a time when Beijing’s overseas ports financing and its other maritime activities are top of mind for policymakers, particularly in the United States. In addition to likely being the world’s top financier, builder, and operator of overseas ports, China is the world’s largest shipbuilder, constructing more than half of all ships (Funaiole et al. 2025). According to CSIS, China’s largest state-owned shipbuilder “built more commercial vessels by tonnage in 2024 than the entire U.S. shipbuilding industry has built since the end of World War II” (Funaiole et al. 2025). In 2025 alone, Chinese yards received orders for 526 new container ships, 371 bulkers, and 276 tankers, with Chinese shipping conglomerate COSCO and its subsidiaries leading the way in terms of orders (Galanopoulos 2026). Both the Trump and Biden Administrations have viewed China’s expanding maritime footprint as a growing strategic and economic challenge, prompting a series of investigations, legislative measures, and policy efforts aimed at understanding the risks and strengthening U.S. alternatives. The 2026 National Defense Authorization Act (NDAA), which became law in December 2025, called for the U.S. Departments of State and Defense to gather information on China’s control over global strategic ports; the U.S. national security and economic implications of Chinese-controlled strategic ports; and measures the U.S. government could take to ensure open access and provide alternatives to Chinese investment in these ports (U.S. Congress 2025–2026). Earlier, in 2024, the U.S. Trade Representative launched an investigation of China’s acts, policies, and practices targeting the maritime, logistics, and shipbuilding sectors for dominance. A subsequent report released in 2025 stated that China’s targeting of the maritime, logistics, and shipbuilding sectors for dominance was “unreasonable and burdens or restricts U.S. commerce and thus is actionable.”

Using data and evidence, Anchoring Global Ambitions sheds light on the true scale and scope of China’s state-directed investments in ports and harbors worldwide. It drills down into the specifics of Beijing’s overseas ports financing and explores the implications for China, the U.S. and its allies, and the countries that receive this financing. It also highlights some of the policy options that powers large and small have before them, as they contemplate the changing global maritime order.

For various reasons, accessing information on China’s overseas lending and grant-giving activities is becoming more difficult, and Beijing increasingly uses opaque and complex borrowing arrangements and financial instruments (Gelpern et al. 2023, 2025a, 2025b; Parks et al. 2025a). Despite these challenges, AidData will continue to track Chinese financing for ports infrastructure worldwide and conduct rigorous policy analysis and peer-reviewed research on its impacts, disseminating this information widely.[4]

2. Where has Beijing directed its overseas financing for ports and equipment?

By Rory Fedorochko, Sheng Zhang, and Seth Goodman

This report and the associated CPORTS 2.0 dataset present the clearest picture yet of the universe of seaport infrastructure and equipment projects financed via loans and grants from Chinese state-owned entities between 2000 and 2025. This analysis excludes ports that are solely funded via equity investments through privately-owned or state-owned Chinese entities—though the bundling of aid, debt, and equity can be an important factor in understanding a given project’s development and intentions.

This chapter begins with a brief overview of the underlying data collection and coding methods.[5] Over a three-year period, the authors used a combination of automated and manual screening techniques to assemble the CPORTS 2.0 dataset. First, a systematic review was conducted of AidData’s CLG-Global 1.0 dataset, which captures 33,580 projects and activities across 217 countries supported by grants and loans from more than 1,100 official sector institutions in China worth nearly $2.2 trillion (in 2023 U.S. dollars) from 2000 to 2023 (Parks et al. 2025b; Dreher et al. 2022). A string detection technique was used to identify a subset of port and port equipment finance records for potential inclusion. A manual review of each “candidate” record was then conducted to eliminate false positives, and coders assigned values to a number of bespoke variables, including the precise name of the port, the type of port, the activity being financed, and the presence of Chinese owners or operators. The research team also collected supplemental data on grant and loan commitments for port projects in 2024 and 2025, extending the time frame covered.

These screening procedures and additional searches identified 363 unique Chinese-financed projects worth $23.9 billion at 168 unique ports across 90 countries from 2000 to 2025. 159 projects supported by commitments worth $10.8 billion are located in high-income countries (HICs), while 204 projects supported by commitments worth $13.1 billion are located in low- and middle-income countries (LMICs).

A previous report, Harboring Global Ambitions, and the earlier CPORTS 1.0 dataset only considered China’s official sector financing for port construction and operations (Wooley et al. 2023). It excluded financing for port equipment, such as the donation of container scanners, in order to focus solely on Chinese financing for deepwater ports that have dual-use (civilian-military) capabilities.

For the present analysis, the scope of inquiry was expanded to include Chinese loans and grants that financed the acquisition of port equipment. In some cases, Chinese financing supported both port construction and equipment acquisition at the same location. Figure 2 below maps China’s total financial commitments for ports worldwide, aggregating lending and grant-giving by port. Table 1 below presents the top 20 Chinese-financed ports by total commitments, including financing for ports, port facilities, and port equipment. Total commitment values captured here also include purely financial activities related to ports, such as acquisition loans for purchasing ownership stakes in overseas ports.

Figure 2. China’s official sector lending and grant-giving for overseas ports, 2000-2025

Note: Financial commitments are shown in constant 2025 USD. Excluded from this map are those loans that are not recommended for aggregation. Source: AidData’s CPORTS Dataset, Version 2.0.

Table 1. Top 20 Chinese-financed ports, 2000-2025

Rank |

Port |

Country |

Commitment (2025 USD) |

1 |

Hambantota International Port |

Sri Lanka |

$1.97 billion |

2 |

Port of Newcastle |

Australia |

$1.32 billion |

3 |

Autonomous Port of Kribi |

Cameroon |

$1.17 billion |

4 |

Port of Melbourne |

Australia |

$1.14 billion |

5 |

Haifa Port |

Israel |

$1.13 billion |

6 |

Jurong Port Universal Terminal |

Singapore |

$994 million |

7 |

Wiggins Island Coal Export Terminal |

Australia |

$946 million |

8 |

Port of Ashdod |

Israel |

$806 million |

9 |

Port of Caio |

Angola |

$804 million |

10 |

Autonomous Port of Abidjan |

Côte d’Ivoire |

$792 million |

11 |

Port of Bata |

Equatorial Guinea |

$733 million |

12 |

Queen Elizabeth II Quay [6] |

Sierra Leone |

$682 million |

13 |

Port of Piraeus |

Greece |

$660 million |

14 |

Lekki Deep Sea Port |

Nigeria |

$635 million |

15 |

Port of Chancay |

Peru |

$631 million |

16 |

Gwadar Port |

Pakistan |

$522 million |

17 |

Porto Paranaguá |

Brazil |

$483 million |

18 |

Autonomous Port of Nouakchott |

Mauritania |

$444 million |

19 |

Doraleh Multipurpose Port and Damerjog Livestock Port [7] |

Djibouti |

$418 million |

20 |

Port of Tema |

Ghana |

$398 million |

Source: AidData’s CPORTS Dataset, Version 2.0.

As Figure 3 below illustrates, approximately 35% of port and/or port facility projects financed by Chinese official sector agencies also involve Chinese port ownership and/or operational control. Disaggregating this figure provides additional clarity. Of the total sample, 20% of projects involve both a Chinese port owner and operator, 6% involve a Chinese owner only, and 9% involve a Chinese operator only. In aggregate, 29% of projects include at least a Chinese operator (whether or not ownership is also present), while 26% involve a Chinese owner. This distribution suggests that Beijing’s priority may extend beyond equity ownership toward securing operational control. To be sure, there are potential negative aspects to this, for both port-hosting nations as well as China’s rivals: operating rights confer significant practical authority, including control over scheduling systems, berth allocation, logistics coordination, and day-to-day port management. In many cases, Chinese SOEs that obtain operating rights are positioned to influence shipping routes, prioritize affiliated carriers, and adjust traffic flows in ways that align with broader commercial or strategic objectives. When combined with ownership stakes, these operational roles can amplify leverage, deepen long-term commercial integration, and enhance strategic influence over maritime trade corridors.[6][7]

From a policy perspective, the relatively high proportion of projects involving Chinese operators (29%) indicates that operational control is not incidental but appears to be a deliberate component of China’s port engagement model. The combination of financing, ownership, and especially operational control may therefore create layered forms of influence that extend beyond traditional infrastructure investment.

Figure 3. Breakdown of Chinese-financed seaport projects by Chinese entity involvement, 2000-2025

Source: AidData’s CPORTS Dataset, Version 2.0.

Table 2 presents the ports and facilities where both Chinese owners and operators are present. There is notable overlap with the most heavily financed ports in Table 1, indicating that many ports are not only significant in terms of total financing commitments but also involve a high degree of ownership and operational control by Chinese entities. Many of these ports or port facilities are strategically positioned along key sea lines of communication (SLOCs), including concentrations of investment in the Indian Ocean and the Red Sea, as well as in the Gulf of Guinea, where Beijing seeks to connect and safeguard the mineral supply chains and critical infrastructure in West Africa where it has invested heavily. (For more on how China’s maritime strategy increasingly emphasizes investments in hubs of connectivity, see Chapter 4).

Table 2. Financing for ports and port facilities with both Chinese owners and operators, 2000-2025

Port |

Country |

Commitment (2025 USD) |

Haifa Port |

Israel |

$1.13 billion |

|

Hambantota International Port |

Sri Lanka |

$980 million |

Port of Newcastle |

Australia |

$667 million |

Port of Piraeus |

Greece |

$660 million |

Lekki Deep Sea Port |

Nigeria |

$634 million |

Port of Chancay |

Peru |

$631 million |

|

Wiggins Island Coal Export Terminal |

Australia |

$620 million |

|

Doraleh Multipurpose Port and Damerjog Livestock Port |

Djibouti |

$418 million |

Port of Boffa |

Guinea |

$91 million |

Khalifa Port |

United Arab Emirates |

$64 million |

Nouadhibou Fishing Port |

Mauritania |

$59 million |

Port of Melbourne |

Australia |

$44.9 million |

PLA Support Base |

Djibouti |

$20 million |

Laem Chabang Port |

Thailand |

N/A |

Note: Financial values in this table capture commitments made only when a Chinese port owner and operator was present.[8] The precise size of the loan commitment for Laem Chabang Port is unknown. Source: AidData’s CPORTS Dataset, Version 2.0.

The financiers and recipients of China’s official sector grant and loan commitments for ports projects have shifted considerably since 2000, as Table 3 demonstrates. Nonetheless, some constants remain. Australia has always been one of the largest recipients of seaport finance, and Africa is always represented. While Chinese policy banks’ prominence has decreased while state-owned commercial banks have gained, the policy banks remain an important component of finance—just no longer in the dominating fashion they enjoyed before 2018.

Table 3. Chinese ports financing by top funding agencies and recipient countries, 2000-2025

Period |

Top three funding agencies |

Top three countries of activity |

2000-2013 (Pre-BRI) |

|

|

2014-2017 (Early BRI) |

|

|

2018-2025 (Late BRI) |

|

|

Source: AidData’s CPORTS Dataset, Version 2.0.

China’s official sector grant and loan commitments- support multiple kinds of port infrastructure, ranging from the construction of entirely new ports and terminals to the extension of piers and berths. Two new qualitative variables were added to the CPORTS 2.0 dataset to enhance analysis: a port facility type variable and a port facility purpose variable.

The port facility type variable seeks to identify what types of physical infrastructure Chinese financing is supporting, such as a terminal, pier, berth, or industrial park. The most common type of construction efforts at ports were for terminals, supporting 35 ports across 58 projects and activities in $9.5 billion of commitments. Construction efforts for more broader works at ports was the second-most common type of port facility financed, supporting 22 seaports across 36 projects and activities in $6.1 billion of commitments.

The port facility purpose variable categorizes the larger purposes of the port facility, such as whether a port primarily serves general cargo and container traffic or was specifically designed to facilitate the export of a specific commodity like liquefied natural gas (LNG) or coal. China’s seaport lending and grant-giving portfolio places great emphasis on supporting the general cargo and container traffic operations of ports—48 ports in 100 projects and activities worth $14.2 billion with general cargo and containers as their purpose. Furthermore, mineral and energy infrastructure is a focus, with finance supporting 13 ports across 31 projects and activities via $3.7 billion in commitments.

It is no accident that mineral and energy infrastructure enjoys a privileged place in China’s official sector financing of seaports. Following the adoption of “BRI 2.0” reforms that began in 2018, China’s state-owned commercial banks have assumed an increasingly important role (see Table 3 below)—via increasingly complex financial arrangements—in expanding Beijing’s control over key segments of the global supply chain for critical minerals (Parks et al. 2023; Escobar et al. 2025). Beijing also appears to be aligning its strategy for ports and port facilities with these changes by focusing its port investments alongside these commodities, discussed at greater length in Chapter 4. Table 4 demonstrates that many of the top 10 ports and port facilities financed during the BRI 2.0 era appear to follow this model.[9] It also highlights a strong focus on the Gulf of Guinea, South America, and Australia.

Table 4. Top 10 Chinese-financed ports during the late BRI, 2018-2025

Port |

Country |

Commitment (2025 USD) |

Lekki Deep Sea Port |

Nigeria |

$635 million |

Port of Chancay |

Peru |

$631 million |

Port of Newcastle |

Australia |

$509 million |

|

Hambantota International Port |

Sri Lanka |

$489 million |

|

Wiggins Island Coal Export Terminal |

Australia |

$326 million |

|

Queensland Curtis LNG Common Facilities |

Australia |

$315 million |

Port of Melbourne |

Australia |

$305 million |

Jurong Port |

Singapore |

$251 million |

Port of Duqm |

Oman |

$227 million |

Port of Valencia |

Spain |

$190 million |

Source: AidData’s CPORTS Dataset, Version 2.0.

Figure 4 is a useful, recent example of the before-and-after results of Chinese financing one port: Lekki Deep Sea Port in Nigeria, today one of West Africa’s most important commercial container hubs. China Development Bank (CDB) provided a $629 million loan for Lekki Deep Sea Port in 2019.[10] China Harbor Engineering Company Ltd. began construction in 2020 and held a stake in the port operator after construction was completed in 2022. Figure 4a shows the site of the Lekki Deep Sea Port in 2019 prior to development activities, while Figure 4b shows the operational port two years after completion in 2024. Visible elements include a substantial breakwater for port protection and multiple berths and cranes at the container terminal.

Figure 4a. Lekki Deep Sea Port in 2019, prior to development

Figure 4b. Lekki Deep Sea Port in 2024, after opening in 2023

Sources: Imagery in Figures 4a and 4b by CNES/Airbus (2025) and Google Earth.

2.1 Chinese-financed ports in high-income countries

Beyond providing four additional years of coverage, the CPORTS 2.0 dataset captures the full range of Chinese official sector loans and grants for ports in high-income countries (HICs), including the United States, Australia, and the EU, thus permitting a truly global analysis of China’s global seaports footprint. A key finding from Chasing China: Learning to Play by Beijing's Global Lending Rules is that HICs are an integral part of Beijing’s overseas lending and grant-giving portfolio (Parks et al. 2025a). China’s financial support for ports in HICs is no exception: 45.1% of its total ports portfolio (worth $10.8 billion) supports 29 port locations[11] and a number of port companies in 20 HICs across a wide variety of geographic regions (see Table 5 below), as well as pledges for four ports in three countries and financing for various port companies. Beijing’s financial commitments range from modest grants for drydocks in Malta to syndicated loans worth tens of millions of dollars for the construction of a new container terminal in the UAE.

China’s seaport financing activities in developed economies support many of the same goals as those in developing economies: boosting Chinese exports, facilitating imports of essential raw minerals, promoting the commercial interests of Chinese companies, and seeking profits for banks. Yet its seaport financing in HICs takes on different forms. For one, financial support for physical construction or the provision of equipment is considerably less prevalent. Only 50.4% of China’s HIC portfolio supported port construction or equipment acquisition, as compared to 86.7% in its LMIC portfolio. With a wealth of existing and mature port assets in HICs—and greater skepticism over wholescale Chinese investment in critical infrastructure—there are fewer opportunities for financing greenfield port construction. However, there are still opportunities to make inroads in HICs. In developed economies, Beijing has focused its efforts on (a) merger & acquisition (M&A) loans that help Chinese investors purchase equity stakes in ports and port companies; and (b) the provision of liquidity support (for general corporate or refinancing purposes) to ports and port companies, which helps ensure the smooth operation of port facilities.[12]

Table 5. Top 20 Chinese-financed ports in high-income countries, 2000-2025

Rank |

Port |

Country |

Commitment (2025 USD) |

1 |

Port of Newcastle |

Australia |

$1.32 billion |

2 |

Port of Melbourne |

Australia |

$1.14 billion |

3 |

Haifa Port |

Israel |

$1.13 billion |

4 |

Jurong Port |

Singapore |

$994 million |

5 |

Wiggins Island Coal Export Terminal |

Australia |

$946 million |

6 |

Port of Ashdod |

Israel |

$806 million |

7 |

Port of Bata |

Equatorial Guinea* |

$733 million |

8 |

Port of Piraeus |

Greece |

$660 million |

9 |

Queensland Curtis LNG Common Facilities |

Australia |

$315 million |

10 |

Port of Duqm |

Oman |

$227 million |

11 |

Port of Valencia |

Spain |

$190 million |

12 |

Port Botany and Port Kembla [13] |

Australia |

$179 million |

13 |

Muara Port |

Brunei Darussalam |

$128 million |

14 |

Napier Port |

New Zealand |

$104 million |

15 |

Port of St John's Antigua |

Antigua and Barbuda |

$96 million |

16 |

Ust-Luga Commercial Sea Port |

Russia |

$85 million |

17 |

Port of Tauranga |

New Zealand |

$73 million |

18 |

Khalifa Port |

United Arab Emirates |

$64 million |

19 |

Port of Long Beach |

United States |

$62 million |

20 |

Lyttelton Port |

New Zealand |

$55 million |

Note: Equatorial Guinea was classified by the World Bank as a high-income country between the years 2007 and 2014. It was later reclassified to upper-middle-income status. As such, it is included in this report’s analysis of HIC ports. Source: AidData’s CPORTS Dataset, Version 2.0.

While these types of financial support draw less attention than financing for brick-and-mortar activities, they are particularly important for the operation and control of port assets.[13] In particular, M&A loans and liquidity support facilities from Chinese state-owned entities can give compatriot firms the initial cash to establish footholds in far-flung places and then maintain their investments over time. 61.6% of China’s official sector M&A lending and liquidity support commitments in HICs supported ports with Chinese or Hong Kong owners or operators.[14] These are rarely one-off transactions; rather, they are provided as recurring support over an extended period of time. Consider Chinese seaport finance at the Port of Melbourne, Australia's largest container and general cargo port. As part of its 2016 privatization by the Victorian state government, a consortium of institutional investors and funds—including China Investment Corporation (Beijing’s sovereign wealth fund)—acquired a 50-year concession and lease over the port’s 35 commercial berths, 515-hectares of land, shipping canals, and other assets. To finance the deal, the consortium borrowed over A$9.7 billion from a syndicate of lenders including Bank of China (BOC), China Construction Bank, and the Industrial and Commercial Bank of China (ICBC). Later, in 2019, a trio of Chinese state-owned lenders participated in another syndicated loan to partially refinance some of the debt the consortium contracted during the initial privatization, and in 2024 further group of Chinese state banks take part in a A$500 million facility for the port’s refinancing and working capital needs. There is little doubt that China Investment Corporation’s stake contributed to the Chinese state banks’ long-term support of the port.

However, Chinese or Hong Kong presence at a port is not required to attract Chinese state capital. In 38.7% of Beijing’s official sector M&A lending and liquidity support commitments for ports in HICs, no Chinese or Hong Kong owners or operators were involved. Such activities range from supporting Macquarie Infrastructure Partners’ acquisition of a 80% stake in the Long Beach Container Terminal in California to the provision of a liquidity support facility to the Port of Brisbane in Queensland, Australia.[15] Some of these ports benefit from long-term support; Napier Port in New Zealand, for example, received NZ$120 million in ICBC lending in 2019 for the 6 Wharf Expansion Project, a berth renovation, and later benefited from a NZ$80 million facility from ICBC in 2025 for refinancing and general corporate purposes. Though ports like Long Beach or Brisbane can have great commercial and strategic significance, these transactions involve only Chinese actors at the financing stage; there is little empirical evidence to suggest that China is pursuing or securing any geostrategic advantages through these investments—rather, the apparent motive is financial profit.

While there is a fair degree of coherence and consistency in China’s overseas seaport financing portfolio in HICs, there are some sources of regional variation that merit further exploration. 43.8% of China’s aid and credit commitments for seaport activities in HICs supported Australia and Oceania, while 23.9% supported activities in the Middle East. 10% supported activities in Europe. The following subsections dives deeper into each region.

2.1.1 Regional focus: Oceania and Australia

While Oceania was the largest regional beneficiary of China’s official sector financial commitments for seaport projects in HICs between 2000 and 2025, it was almost entirely driven by one mammoth recipient: Australia. In fact, the country is the single largest recipient of Chinese seaport financing worldwide, with $4.5 billion supporting seven ports: Port Botany and Port Kembla, Brisbane, Hay Point, Newcastle, Melbourne, Queensland Curtis, and Wiggins Island at Gladstone. There were also pledges of financial support for another two ports that never reached the formal commitment stage: Darwin and Oakajee. Of note, Australia is also the world’s third-largest recipient of all official sector lending and grant-giving from China: $130.7 billion from 2000 to 2023 (Parks et al. 2025a). China’s seaport financing activities in Australia have generally supported efforts to secure raw minerals, and especially coal and iron. These include the Wiggins Island Coal Export Terminal and the terminals at the ports of Newcastle and Hay Point. Even though China is both a major importer of Australian minerals and its companies have a substantial presence in the Australian mining sector (i.e. the Sino Iron Project and Karara Iron Ore Project, both of which were heavily supported by Chinese state-owned banks), Chinese owners and operators have only a small presence at mineral-oriented seaports that actually received Chinese seaport finance. Only one, the Yancoal-minority owned Newcastle Coal Infrastructure Group (NCIG) Export Terminal at the Port of Newcastle in New South Wales—where China Merchants Port Holding Company is an operator—has Chinese ownership.

Even beyond mineral-focused ports, Chinese ownership and operatorship in Australia is limited. That said, ports with ownership or operatorship by Chinese or Hong Kong entities—Newcastle, Melbourne, and Wiggin Islands—received substantial funding, with some $3.4 billion in total financial commitments.

Chinese involvement in these Australian ports has largely avoided controversy, as activities appear primarily commercial in interest and limited to financing. However, because of its security implications, Chinese activity at Darwin Port in the Northern Territory has been a long-standing source of heated debate in Australia. The facility’s northern location puts it in close proximity to key Indo-Pacific shipping routes. Private Chinese company Shandong Landbridge acquired a 99-year lease at Darwin in 2015, with plans to develop a hotel and logistics base at the site.

The deal quickly became controversial. Then-U.S. President Barack Obama criticized the lease and claimed that the U.S. government had little time to register its concerns with the Australian government. American officials worried that Chinese port access to Darwin would facilitate espionage on the nearby U.S. Marine Corps presence (Coorey and Tingle 2015). Landbridge denied any ulterior motive. Lesser known is that Landbridge, circa 2017, sought a A$500 million loan from China Eximbank to support redevelopment at the port. That loan was ultimately never finalized. Darwin has remained a point of contention as recently as January 2026, with plans by the government of Anthony Albanese to force Landbridge out of the lease, which in turn drew threats from Chinese officials (McIlroy 2026). Nonetheless, other sources of seaport financing to Australia have persisted with a port portfolio that appears largely commercial in orientation—none of the ports funded by official Chinese agencies or entities are geographically proximate to Australia’s AUKUS industrial or operational bases, which have been concentrated to date around Perth and Adelaide, or have attracted much scrutiny outside of Darwin, and the minimal Chinese ownership and operatorship speaks to Chinese banks simply seeking out profits by lending to ports.

Australia’s neighbor, New Zealand, has also been a recipient of official sector credit from China, with some $232 million for three ports: Napier, Lyttelton, and Tauranga. While not comparable in scale to its financial footprint in Australia, Chinese seaport financing in New Zealand is not insignificant; the size of the bank syndicates that provide loans to these ports are small—ranging from two to five banks—meaning that Chinese state-owned creditors play outsized roles in bankrolling the construction and operation of these ports.[16] None of these ports have Chinese or Hong Kong ownership or operatorship, suggesting that, like in Australia, Chinese banks’ goal is profit-seeking.

2.1.2 Regional focus: The Middle East

The second largest high-income regional beneficiary of China’s seaport financing commitments is the Middle East, with $2.6 billion supporting five ports—Haifa and Ashdod in Israel, Khalifa in the United Arab Emirates, New Doha Port in Qatar, and Duqm in Oman—as well UAE-based global port and terminal operator AD Ports Group. This pattern tracks with the wider deepening of economic relations between China and the Middle East. Between 2018 and 2023, China showered the broader Middle East with financial support: six of the twenty largest recipients of official sector credit were Saudi Arabia, the United Arab Emirates, Turkey, Iraq, Iran, and Egypt (Parks et al. 2025a: 154). If one broadens the aperture to include the LMICs, China’s deep interest in the region's connective infrastructure becomes even more apparent: China’s seaport financing portfolio has supported facilities in Iraq, Lebanon, Syria, Yemen, and Turkey. Add into the mix Gwadar, in Pakistan’s far west, terminus to the China-Pakistan Economic Corridor, located on the Gulf of Oman and within a short sail to the Strait of Hormuz and the geographic linkages of these assets is apparent.

Economic considerations are no doubt a factor in these projects, as supporting ports facilitates the oil and gas trade that is important to China. Some 50% of China’s crude oil imports come from Gulf countries and 29% of its LNG imports come from Qatar and the United Arab Emirates, most of which must pass through the geostrategic Strait of Hormuz. Long-term disruptions of maritime traffic through this critical strait would cause economic pain for Beijing (Soni and Allen 2026; Corbeau and Erica Downs 2025). It is thus no surprise that the Middle East is one of the few areas where Beijing has taken tangible, public steps to establish a long-term naval presence. Its first overseas naval base in Djibouti—created nominally for anti-piracy efforts off of Somalia and after Chinese entities had invested in the nearby Doraleh Multipurpose Port—provided Beijing with the ability to have a permanent presence at the Bab-el-Mandeb, Gulf of Aden, and further up the Red Sea and to facilitate power projection across the Indian Ocean (Sun and Zoubir 2021). A naval base located within the strategic Persian Gulf itself would dramatically enhance its abilities to protect its seaborne lines of communication and its capacity to directly influence geopolitics in the region (Mazzucco 2025). Being able to sustain naval activity in the region, coupled with good ties with the region’s governments, also provides China with other benefits. In 2023, when Sudan fell into civil war, two PLAN vessels conducting escort missions in the Gulf of Aden evacuated hundreds of Chinese and foreign nationals from Port Sudan to the Port of Jeddah in Saudi Arabia, simultaneously safeguarding Chinese citizens and providing a valuable service for other countries (Ministry of National Defense 2023). With looming instability in the Middle East, China’s support of port infrastructure in the region may help facilitate more naval presence, protecting its supply chains.

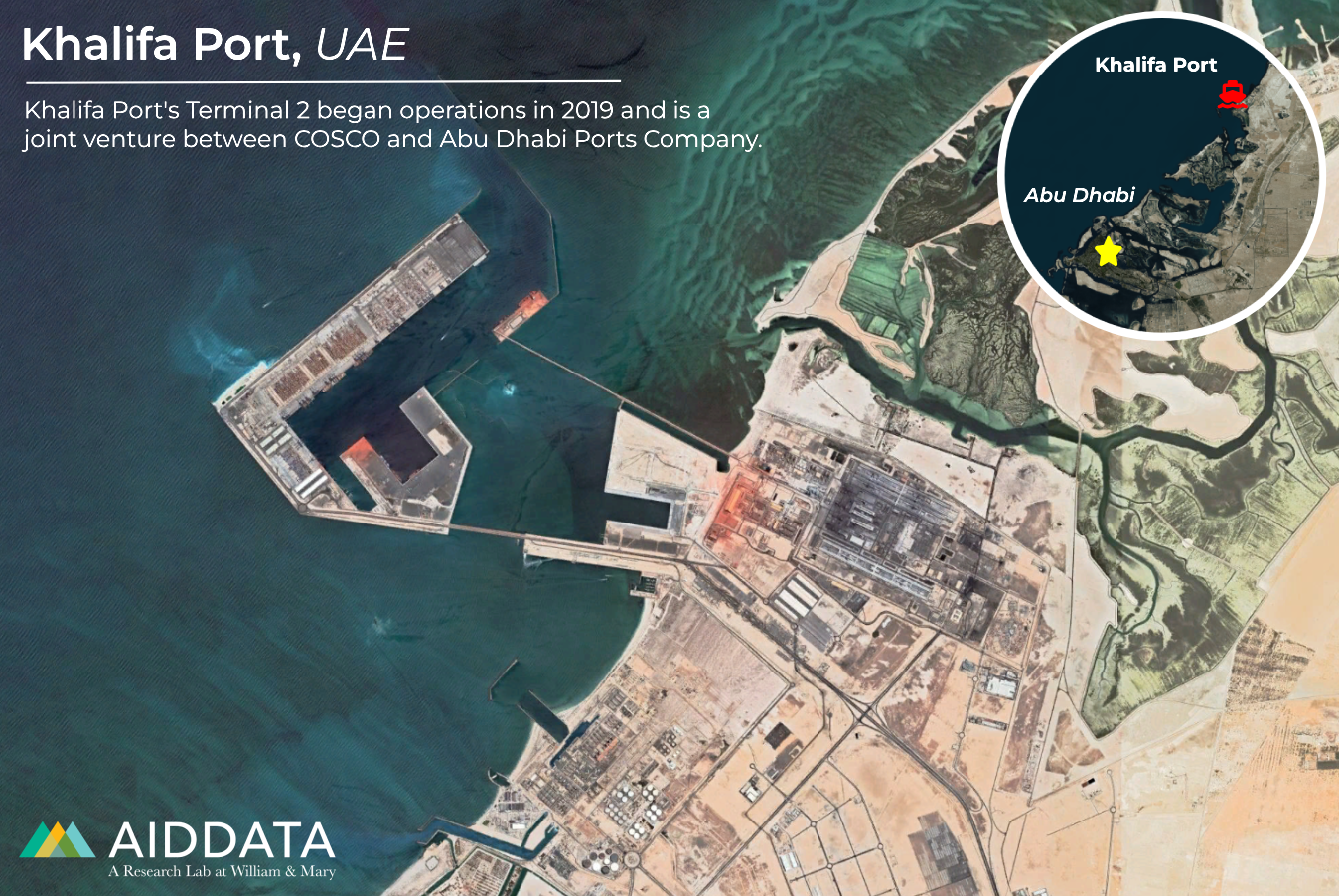

Khalifa Port, in Abu Dhabi in the UAE, merits special scrutiny in this respect. In 2018, Bank of China, together with three other lenders, provided a $260 million loan to a 90:10 joint venture between COSCO and Abu Dhabi Ports Company to construct Khalifa Port Container Terminal 2 (also known as CSP Abu Dhabi Terminal), a three-berth, 2.4 million twenty-foot equivalent unit (TEU) terminal. COSCO obtained a 35-year concession with hopes to transform Khalifa into the Middle East’s next hub port. The project attracted substantial interest from a diverse range of Chinese state-affilitated actors. China’s National Development and Reform Commission “initiated and coordinated” the terminal project as part of the Belt and Road Initiative (ICBC n.d.). Besides COSCO’s equity stake in the terminal—only the second foreign terminal where it held controlling ownership—the joint venture hired several Chinese state-owned contractors to be involved in construction. China Harbour Engineering Corporation and CCCC First Navigation Engineering Bureau laid steel rails at the pier, helped automate the terminal, and constructed ancillary facilities; SinoPro provided steel and other construction supplies, and Shanghai Zhenhua Heavy Industries supplied 43 cranes. Operations at the terminal began in 2019.

In late 2021, allegations of non-commercial Chinese interests spilled into public view. That spring, the U.S. intelligence community assessed, based on reports and satellite imagery of Khalifa, that China was constructing a secret military installation within the terminal (Lubold and Strobel 2021). The assessment led to a flurry of diplomatic efforts by American officials to convince the Emirates of the facility’s military intent and potential consequences for US-UAE relations (Lubold and Strobel 2021). This included two phone calls between then-U.S. President Joe Biden and Abu Dhabi Crown Prince Mohamed bin Zayed al Nahyan. Besides the broad potential strategic impact, Khalifa’s relative proximity to sensitive sites—Jebel Ali Port, a port that hosts U.S. Navy goodwill and replenishment visits, and al-Dhafra Air Base, home to the American and French militaries—made the risk especially salient for policymakers in the United States (Mazzucco 2025). After the American pressure campaign, construction at the site halted in fall in 2021, and the UAE allowed American officials to inspect the site. The Emirati government denied ever considering hosting the Chinese military, in Khalifa or elsewhere.

The alleged attempt to build a military facility at Khalifa is consistent with concerns that Beijing has an interest in expanding its naval presence in the Middle East beyond its base in Djibouti, providing it with strategic depth and breadth to support its foreign policy agenda in the region. Nonetheless, a larger footprint is not without risk; a Chinese base would leave it directly exposed to regional disputes and crises, potentially forcing it into unwanted entanglements that endanger the powerful commercial considerations that motivate much of China’s financing of seaports. Given its strategic location and the continued importance of its fossil fuels to the Chinese economy, the Middle East will likely continue to attract Beijing’s seaport investments for the foreseeable future.

Figure 5a. Khalifa Port in 2016, prior to Chinese-financed development

Figure 5b. Khalifa Port in 2021, after Terminal 2’s opening in 2019

Sources: The imagery in Figures 5a and 5b is by Vantor (2025) and Google Earth.

2.1.3 Regional focus: Europe

China’s financial commitments for seaport projects in European HICs totalled $1.1 billion across six ports: the Malta Drydocks and the Malta Freeport, Sabetta and Ust-Luga in Russia, Piraeus in Greece, and, most recently, Valencia in Spain. These commitments also supported two port companies: United Kingdom-based PD Ports, a port operator and owner focused on England, with some operations at the country’s largest port container port, Felixstowe, and Europe Container Terminal B.V., a Netherlands-based firm affiliated with Hong Kong-based CK Hutchison Holdings that has operations at the Port of Rotterdam and other ports. Chinese and Hong Kong companies are well-known European port operators and owners, playing key roles in the region’s connective infrastructure, with significant footprints in Hamburg in Germany and Antwerp in Belgium, among others. However, these investments are not known to have benefited from loans or grants from China’s official sector agencies (which often offer generous terms for Chinese companies making large overseas investments) and thus are not included in the CPORTS 2.0 dataset. However, the most well-known Chinese port investment in Europe—the Port of Piraeus in Greece—did benefit from such activity.

CDB issued two loans worth $551 million to support Chinese state-owned COSCO Shipping Ports’ acquisition and renovation of Pier II and III of Piraeus Container Terminal under a 30-year build-operate-transfer concession. Under the terms of the initial agreement, COSCO increased the throughput capacity of the container terminal to 3.7 million TEUs. COSCO's concession was a major success, leading to one of the largest increases in TEU handling in all of Europe by 2016, where Piraeus was the eighth largest container port by TEU (Glass 2017). In 2016, COSCO later acquired a 51% ownership stake in the Piraeus Port Authority from the Greek government, which grew to 67% in 2021 after COSCO made hundreds of millions of euros in mandatory investments (Koutantou 2021). In an article in Greek newspaper Kathimeriní just prior to his November 2019 visit to Greece—which included a stop at the Port of Piraeus—Xi Jinping called the port the “dragon’s head” for Chinese investment in Greece and pointed out the port’s success as one of the largest in the Mediterranean (Kathimeriní 2019). In Europe, Chinese SOEs tend to be minority shareholders, though in some cases enough shares to block or affect corporate decisions. Piraeus is a notable exception, with COSCO exercising full control over both of its terminals and the port authority itself—though it took years for it to achieve those powers (Popławski 2025).[17]

Brent Sadler, a Senior Research Fellow in Naval Warfare and Advanced Technology at the Heritage Foundation's Allison Center for National Security, has argued that the U.S. can more effectively work with its allies to marry trade with security, ensuring access to needed shipping and ports in crisis and conflict. In Greece, he has advocated for opening ports like Elefsina to facilitate greater energy trade, gain access to a naval repair facility, and mitigate potential interference by Chinese entities at their nearby Port of Piraeus (Sadler 2025b).[18]

Chinese influence over ports in Europe, whether at Piraeus or other sites where Chinese and Hong Kong companies have ownership and operatorship, have spurred increased strategic and security concerns, including specific worries about espionage linked to hardware and software provided by such entities. More broadly applicable are the economic implications of China’s port presence in Europe. These countries are important trade partners for China and streamlining trade—both via physical port infrastructure and the economic and diplomatic cooperation that comes with port operatorship—remains a major incentive for Chinese companies to engage with Europe in the ports space.

3. Chinese-financed port equipment: Linking hardware and software

By Lea Thome

This report and the associated CPORTs 2.0 dataset capture, for the first time, Chinese state-directed financial commitments for shoreside port equipment—key components that are often closely integrated into Chinese-financed ports. The machinery in question includes scanners, cranes, management software, and forklifts, among others. Together, these activities mutually reinforce Chinese maritime power and demonstrate China’s preeminence as an essential supplier of these tools for global maritime supply chains. By marrying hardware with software, Chinese financiers and suppliers are able to offer “package deals” and build integrated logistics networks that move beyond physical infrastructure to the digital sphere.

The CPORTS 2.0 dataset tracks port equipment across three categories: (1) “customs and security equipment,” such as the containers and truck scanners provided by the Chinese company Nuctech; (2) “ship-to-shore and handling equipment,” such as the cranes provided by Chinese state-owned enterprise Shanghai Zhenhua Heavy Industries (ZPMC) used to onload and offload containers at seaports; and (3) “general equipment provision,” used when specific equipment cannot be identified or when equipment is provided alongside general financing for the construction, extension, and modernization of a port facility.

Although other categories of port equipment exist, including software applications like LOGINK, the CPORTS 2.0 dataset only captures Chinese official sector financing activities, which include grant and loan commitments. Still, LOGINK—a ports logistics platform initially pioneered by Zhejiang’s Department of Transportation and disseminated to ports across the world free-of-charge—highlights the wide-ranging nature of port equipment provided by Chinese agencies and companies.

Figure 6. Chinese official financing for overseas port equipment, 2000-2025

Source: AidData’s CPORTS Dataset, Version 2.0.

Between 2000 and 2025, Chinese financiers directed over $4.7 billion for 102 port equipment projects and activities at 70 seaports worldwide, ranging from the United Arab Emirates and Australia to Peru and the Philippines.[19] However, aid and credit for port equipment is often linked to port facility financing—a port undergoing a modernization may also see the installation of new scanners or cranes. The data shows no clear evidence that Chinese financiers prefer to direct financing for port equipment to ports where Chinese operators or owners are present. Instead, there is an almost even split between ports where Chinese entities are present (49%) and are not (51%).

The Port of Buenaventura in Colombia is a case in point. ICBC and BOC contributed $68.5 million of refinancing support for the Port of Buenaventura’s construction and modernization in 2018; earlier, in 2010, the Chinese Embassy in Colombia provided a grant for on-site installation and use of scanning equipment for shipping containers. In 2024, ICBC contributed a further $33.1 million to Phase 2 of Buenaventura’s expansion project, including the addition of two new ship-to-shore container cranes.

China’s official sector financiers provided $491.3 million in grant and loan commitments for port equipment alone, excluding any projects that also include financing for other port facility infrastructure. However, this number is artificially low, as port facility financing often includes the acquisition of equipment, without identifying how much money is specifically earmarked for this purpose. Port equipment is also much less expensive than port infrastructure, with scanners and cranes typically only accounting for a few million dollars per acquisition.

3.1 What accounts for China’s increased financing of ports equipment?

Two years stand out in China’s seaport equipment financing portfolio: commitments in 2014 account for 40.6% of the portfolio, while commitments in 2023 account for 13.3% of the portfolio.

In 2014, BOC, ICBC, Bank of Shanghai, and Bank of Communications contributed to a syndicated loan for the Bayport Terminal concession project, which supported Shanghai International Port Group’s (SIPG) bid for the concession of the Bayport terminal at Haifa Port. This 25-year concession agreement made SIPG responsible for several components: construction of the facilities at the back terminal; deployment and installation of the port equipment needed to service the port; and daily running and operation of the terminal. In total, these four Chinese state-owned banks provided over $1 billion to support this project.

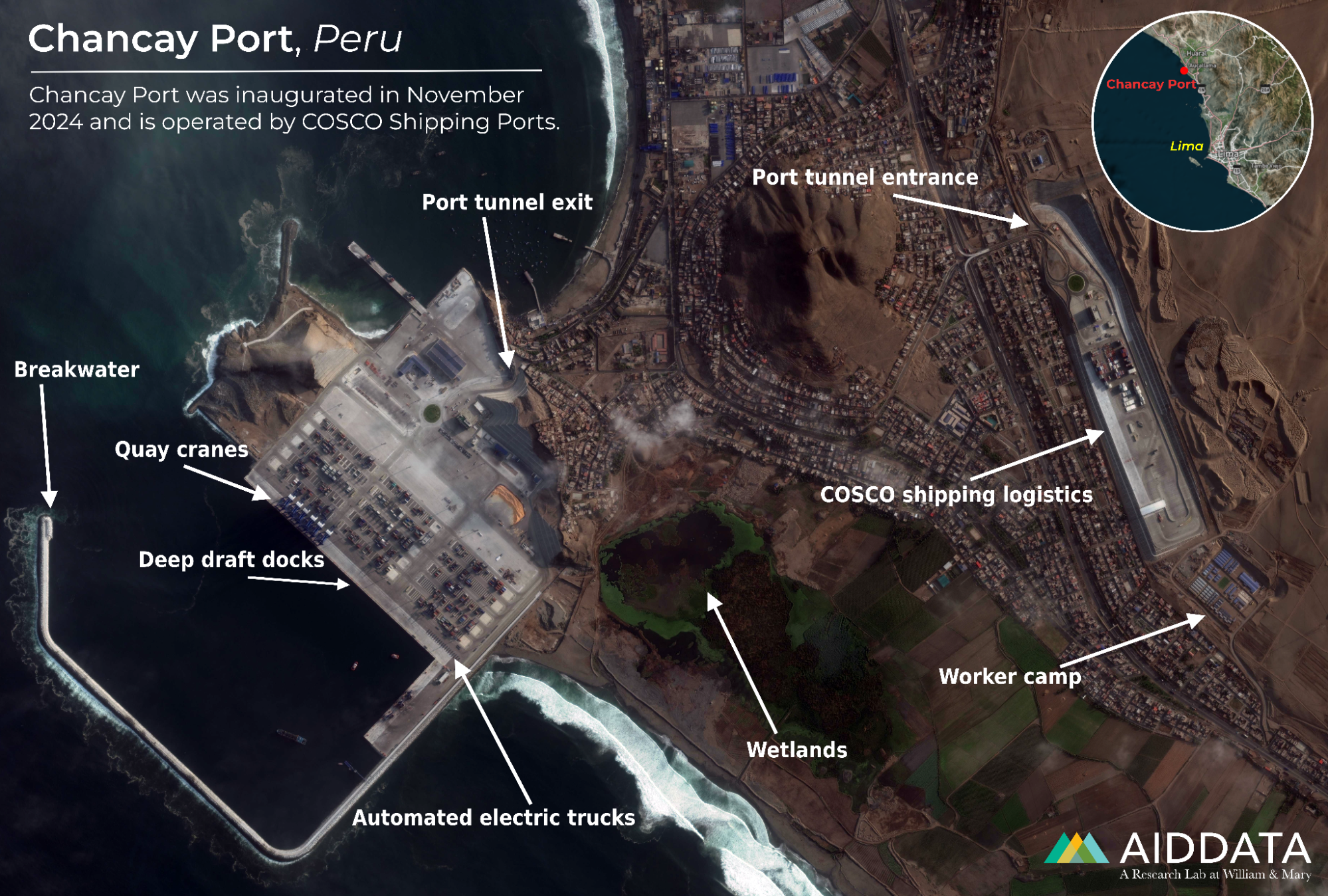

In 2023, one main driver of the spike in financing was the construction of the Port of Chancay in Peru—the first phase of which was completed and inaugurated in November 2024. Five Chinese state-owned banks contributed to a $975 million loan for the construction of the facility. A joint venture of Volcan Compañia Minera S.A.A., a publicly-held mining company in Peru, and COSCO SHIPPING Ports Ltd. COSCO, a state-owned Chinese company that is the second-largest operator of container ports in the world, acquired a 60% stake in the port (Thome 2024). As part of this financing, ZPMC served as an implementing agency and provided equipment, including “five double-cantilever automated rail cranes for the first phase” of the port (Shanghai Zhenhua Heavy Industries Co., Ltd. 2024).

3.2 Which Chinese entities provide port equipment?

Most often, port equipment refers to two primary kinds of machinery: customs scanners, which screen cargo as it enters and leaves the port, and ship-to-shore cranes, which transport cargo from the ship to the shoreside. Chinese companies, such as Nuctech and ZPMC, have established near-monopolies in their respective fields of scanners and cranes, with their products in-service in more than 100 countries around the world.

Figure 7. Chinese official financing for port equipment by type, 2000-2025

Note: “General equipment” and “ship-to-shore and handling equipment” are listed together as the top category, as this general equipment provision cannot be disaggregated when provided together with other kinds of equipment. Source: AidData’s CPORTS Dataset, Version 2.0.

Which kinds of equipment have received the most official financing from China from 2000 to 2025? General equipment alongside port financing emerged as the most-financed form of port equipment by China, with Chinese entities committing almost $1.9 billion in this twenty-six year period. A few of these projects also included ship-to-shore handling equipment alongside general equipment provision (here listed as “General Equipment and Ship-to-Shore and Handling Equipment,” as these cannot be disaggregated), reaching nearly $2.1 billion in financing.

However, when examined by record count, customs and security equipment—such as scanners—are the most common port equipment type identified in the CPORTS 2.0 dataset. These records typically either provide little or no information about the financial value of the equipment for which the grant or loan was obtained. These equipment provisions also tend to be much less expensive than other large-scale port equipment like cranes.

Figure 8. Composition of Chinese port equipment providers by implementing agency, 2000-2023

Note: Approximately $2.4 billion in financing for port equipment that could not be identified to a particular company and is excluded from this chart. Source: AidData’s CPORTS Dataset, Version 2.0.

This analysis also identifies the implementing agencies and providers for 64 port equipment projects and activities supported by financial commitments worth nearly $2.4 billion. Only five companies were responsible for these projects and activities: XCMG, ZPMC, ZPMC Lanka, Nuctech, and Cargotec Oyj.

XCMG served as the implementing agency and equipment provider for two projects supported by grant and loan commitments worth almost $810 million: the Baku International Sea Trade Port Assistance Project in Azerbaijan and the Ashdod Port Southern Terminal Construction Project in Israel. As part of the Baku project, XCMG provided 34 pieces of heavy equipment to the Baku International Sea Trade Port, including 16 forklifts with carrying capacity from 1.5 to 20 tons, two 45-ton telescopic container loaders, three 30-ton trailers for tractors, one 220-ton crane, and other equipment. In addition to the equipment, XCMG dispatched a six-member team to Azerbaijan for a 30-day training and support period.

ZPMC was selected as the equipment provider and implementing agency for projects financed by aid and credit commitments worth $787 million. It supported projects with equipment at the Port of Cotonou (Benin), the Port of Chancay (Peru), Terminal 2 of the Khalifa Container Port (UAE), the Port of Mariel (Cuba), the Rio Grande Container Terminal (Brazil), and the Kingston Container Terminal (Jamaica). While Nuctech has provided comparatively lower levels of port equipment financing ($250 million) than ZPMC and XCMG, it provided the largest number of equipment projects, with at least 44 known activities.

While ZPMC and Nuctech have made the news and drawn scrutiny from legislators in countries such as the U.S., China’s seaport equipment provision and its leading manufacturers and suppliers have generally flown beneath the radar. This analysis represents a first attempt to better understand the wide-scale dissemination of this equipment and its potential implications.

3.3 Why port equipment should be evaluated alongside general port financing